Continental Finance Guide to Understand Your Credit Score, Debt and Income

This guide will help you apply for an unsecured credit card that fits your profile.

The Key Topics of this guide:

- Applying for credit cards with bad credit

- Applying for credit cards with no credit

- Credit card approval odds

- Best credit cards of 2022

Continental Finance, the marketer and servicer of Surge Mastercard, strives to help searchers make sound financial decisions about their credit options and their credit history. To that end, this article is part of a series of guides that will help people on their journey to establish and build good credit.

Let’s start with the most basic: How to apply for and get approved for a credit card.

Applying for a credit card is easy. Most times all you need do is fill out an online form and click the “apply now” button.

But getting approved for a credit card? That can be a whole lot trickier for some people.

1. First, Know What a Good Credit Score is

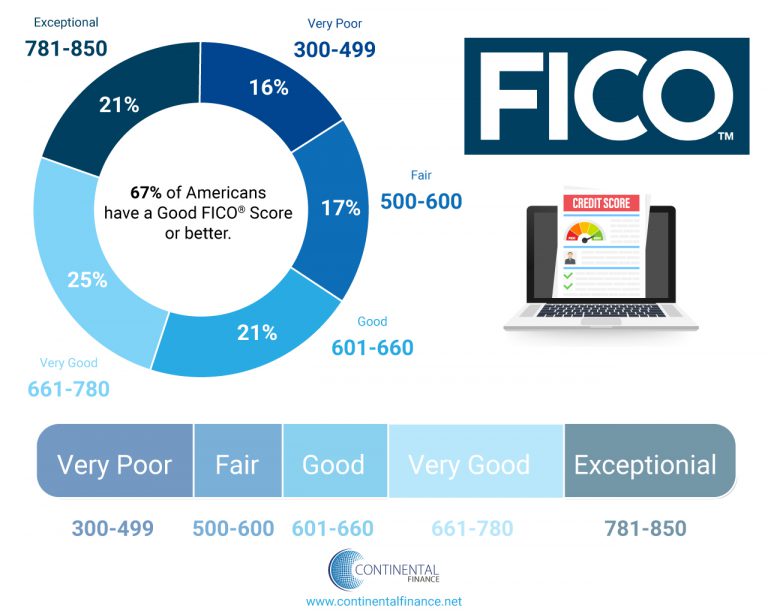

A credit score is one of the single most important factors considered by companies market credit cards when they decide to approve a person’s application. There are a wide variety of credit scores and two of the most popular are FICO Score and VantageScore.

When making a decision on an application, credit card marketers can use different scores or analyze the score or scores differently. But credit scores on average are classified by credit card marketers in tiers like this:

| 300-629 | Poor Credit |

| 630-689 | Average Credit |

| 690-719 | Good Credit |

| 720 and up | Excellent Credit |

These tiers get used by card companies in their decision process. Different cards, with different features typically have a minimum credit score to qualify for the card.

Note: Rewards-based credit cards are extremely popular. People love earning rewards from their card usage.

And most rewards credit cards require good or excellent credit. If you have struggled to maintain a good credit history, or you are just beginning to build your credit history, you might want to delay applying for those kinds of cards until your credit improves.

Or, instead of rewards cards, you could consider secured cards or cards designed for people with bad credit.

2. Next, Know Your Credit Scores

The two most prominent scoring models used by the major credit bureaus are FICO score and VantageScore 3.0. Getting your individual score from these two sources is often very easy.

{kind=link}

{kind=link}

First, FICO Score

You can pay to get your FICO score from MyFICO.com, but if you already have a credit card account, you may also already have access to free FICO scores on your monthly statement or online account.

And Discover, an issuer of credit cards, offers a free FICO score to everybody, even if you’re not a customer.

Next, VantageScore

Some personal finance websites, including Credit Karma, offer a free credit score from VantageScore. Vantage scores and FICO scores track similarly because both weigh many of the exact same factors in their calculation. Also, they tend to use the same data from the credit bureaus.

3. Now, Improve Your Credit

Your credit scores will rise if you:

- Make monthly payments on time.

- Keep balances low on existing credit cards.

- Avoid new debt.

You’ll notice these tips focus on debt and debt management. Approximately 30% of your credit score is determined by how much you owe.

High credit card balances can be especially damaging.

A key factor in building good credit is your credit utilization ratio — which is your balance divided by your credit limit. To improve your credit score and boost your credit profile in the eyes of credit card marketers your credit utilization ratio should be below 30% on each credit card you have.

That means if you have a card with a credit limit of $500, it’s recommended to keep the balance below $150.

To lower your credit utilization, create a plan to pay down an existing balance as quickly as possible. Also, consider paying off purchases more than once a month and paying more than the minimum. Taking actions like those will keep your balance lower throughout the month and send a positive signal that impacts your credit score.

One tactic to be careful of when trying to improve your credit utilization ratio is balance transfers. Make sure you only initiate a balance transfer to a different card when you know it is going to help you manage the payments. It’s better to deal with higher utilization rate than to create a situation where you can’t meet your regular monthly payments.

Pro-Tip: A Credit Rent Boost Could Improve Your Credit Score

Another tip to improve your credit is to provide the credit bureaus examples of your ability to make payments for other bills. Free Rent Reporting can provide a near instant boost to your credit score. This service could take your application from a rejection to an approval with just a few easy steps.

4. Don’t Jump at the First Offer you get

People with no credit are brand new to the game. And people with less than perfect credit may not have fully experienced what happens with credit card offers yet. But one thing to remember is you will see a lot of offers.

That means you can be picky and do not need to jump at the first offer you get.

Each credit card application you fill out will require a check of your credit history. And that means each rejection you get can temporarily ding your credit report. So be wary of the offers you get and do not jump at the first offer you are sent.

Take a moment to read the terms and conditions carefully. If you have less than perfect credit you may not be approved for offers that promise large sign-up bonuses or lucrative rewards.

Consider using an online tool or mobile app to see if you might pre-qualify for an offer. Pre-qualification will ensure you get a card, and avoid any negatives on your credit report just for showing interest in acquiring a card.

Checking takes only a moment, and it will not harm your credit score.

No luck pre-qualifying?

Continental Finance is one of the leading marketers and servicers of credit cards for people with less-than-perfect credit. They market the Surge Mastercard and can help you get closer to reaching your goals through credit over time. This blog and other educational resources will help you learn how to qualify for a card and then use the card responsibly to help mend your credit.

5. Include all Income in Your Credit Application

Companies that review credit card applications consider your credit scores an indicator of your worthiness to be given a card. But scores don’t tell the whole story.

Another important factor is your income. Credit card marketers use income to calculate your debt-to-income ratio. This helps determine your ability to make payments. And card marketers want to ensure they provide credit card offers to people they feel will be able to make the payments.

To change your debt-to-income ratio you need to either increase your income or decrease your debt.

What that means is you can report other sources of income when applying for a credit card. If you earn money outside your full-time job, include that information on your application.

You can include your household income, for example. Which means reporting income from your spouse or partner, on your credit card application.

Just remember to be careful. Resist the temptation to overstate your income. If a credit card marketer finds that you knowingly provided false information on your application, you could be charged and convicted of credit card fraud.

Also note that income is what credit card marketers consider, not employment status. So, being unemployed does not automatically disqualify you from applying for and being approved for a credit card.

6. Don’t Give up After a Rejection

If you think you’ve done everything right and your application is still denied, don’t give up on your quest to obtain good credit.

First thing to do is reach out to the credit card marketer. The company can give you assistance and other options to help you get credit.

Remember to have a plan before you call. Keep these points in mind:

- you have the right to ask the company why you were denied

- you can also check your free credit report at AnnualCreditReport.com

- see if there are any blemishes on your history

- formulate a convincing argument for why you want the card

- prepare reasons for why you are fiscally responsible

- and most of all be polite

Customer service agents are more likely to respond positively if you have a pleasant demeanor.

Still no luck?

If your credit history isn’t perfect, and you have had trouble getting approved for a credit card, remember you are not alone. Improving your credit scores takes time. So the final piece of advice in our guide is to be patient. Waiting between one to three months between credit card applications can increase your chances of getting approved.

The Bottom Line for Obtaining a Credit Line

Credit cards aren’t like debit cards. There is an amazing amount of potential to help your full financial profile through responsible and regular use of credit.

But first you need to get a credit card. Fast and easy application for credit cards are everywhere. But that makes the application process very important.

Being denied for a credit card stings.

It can hurt you psychologically and it can also have a very real and negative impact on your credit score.

So remember it is very important to take stock of your credit profile and before you apply for your next card. Apply for credit with a responsible plan and take action.

- You want to choose the best card.

- You want to be aware of the details like interest rates and any refundable security deposit requirements.

- You want to provide the most accurate information possible.

- You want to have your ducks in a row to make the best case possible.

Take your time, showcase a responsible payment history and be persistent. That’s the key to getting your credit card application approved.

People Also Read

- How to Stay in Your Financial Lane

- Capital One Data Breach: What You Need to Know

- How to Stop Impulse Spending With Your Credit Card

Continental Finance is one of America’s leading marketers and servicers of credit cards for people with less-than-perfect credit. Learn more by visiting ContinentalFinance.net